Free Markets are supposed to fine-tune the synchronization of the Demand for Investment Opportunities with the Supply of Innovative Ideas…

But “Herding Behavior” causes “Coarse Synchronization” which can lead to Chaos in the Financial Markets…

[Note: This article is very long – much longer than I would normally write, it is about 4200 words – but that is because there is a lot in it.]

Part 1 – The Invisible Hand

Adam Smith and the Invisible Hand

In the early 1700’s Adam Smith – the “Father of Economics” – told us of how free markets efficiently self-stabilize – “pulled as if by an ‘invisible hand’” – to the optimal economic equilibrium by the competitive forces of supply and demand. Today we know this isn’t always true. Markets are not always efficient and do not always self-stabilize. Instead they can often create bubbles, recessions, and even depressions.

Over the years, many economists have noted these facts and prescribed a variety of solutions: anti-cyclical government spending, greater regulation and stimulus packages on the one side (Keynes, Saltwater Economists, etc) or austerity and financial husbandry on the other side (Friedman, Austrian School, Freshwater Economists, etc). But the problem is despite the many solutions to market inefficiency nobody has yet answered the question: “WHY do financial markets not correct themselves when they get too high or too low – as Adam Smith said they would?”

The short answer, to this big question, is that; as serendipitous as the natural unfolding of a bountiful economy might seem, it relies heavily on the “efficient” guidance of the invisible hand – but unfortunately efficiency is not always guaranteed!

Part 2 – Complex Equilibrium

Complex Adaptive Economy

Chaos Theory has shown us that there is more to equilibrium than meets the eye. Chaos Theory introduced us to the idea that there can be many different forms of equilibrium, showing us that equilibrium can, in reality, be a multi-dimensional space…

In economics, equilibrium is fundamentally a 2-dimensional space. Trade determines the equilibrium balance of supply and demand, and in so doing drives the Emergence of Economic Integrated Diversity. However it is the amount of investment in new ideas that determines the equilibrium balance of innovation and upheaval which drives the Progressive Evolution to Ever Greater Economic Complexity.

Thus markets are the trade dimension of the economic activity of the agents in the system, and innovation is the complexity dimension of the economic activity of the system as a whole. Markets determine how diversity in the economy is integrated through trade, and the constant interplay of innovative emergence and creative upheaval, evolves the economy to ever greater complexity.

When Adam Smith described the economy as a naturally self-organizing system, he was essentially talking about the complexity dimension of a “Complex Adaptive System”. And when he talked about an invisible hand, what he had essentially identified was that individuals acting in their own self-interest adapt to each other, and, in so doing, the economy as a whole is constantly self-organizing itself to a more complex economic equilibrium. In the concept and use of the phase “invisible hand”, Adam Smith had essentially identified how Complexity Progressively Evolves in the “Complex Adaptive Economy” (CAE).

Spectrum of Equilibrium

Left to itself a CAE will self-organize itself to some form of economic equilibrium; but this is not an equilibrium in the price dimension (dealing with the supply and demand of goods); this is an equilibrium in the complexity dimension (dealing with the emergence and upheaval of innovative diversity).

This complex equilibrium is an evolving, dynamic equilibrium, which might sound to some as a contradiction in terms, but “Chaos Theory” has shown us that equilibrium need not be restricted to the dull and boring, there is in fact is a whole spectrum of possible equilibriums ranging from thermal to chaotic, and the optimal complex equilibrium lies somewhere in between….

“Chaos” is what produces this complexity – but from an economic point of view, there is “Good Chaos” and “Bad Chaos”.

- Good Chaos is “Coarse Symmetry”, which is beneficial for the “Micro-economic Structure” of the economy, because it is what causes the emergence of economic diversity.

- Bad Chaos is “Coarse Synchronicity”, which is not so good for the “Macro-economic Behavior” of the economy because it is what causes the emergence of boom and bust economics.

{kind=link}

Part 3 – The wisdom of crowds

Excess

Economics is often thought of as a study of the allocation of “scarce” resources. But that’s just another way of saying that economics is the study of “people making rational decisions”; and unfortunately we all now know that this is not true. The starting point for all of economics is actually the ability to “produce excess” – and it is this excess productivity that drives both dimensions of a CAE…

In a time before money, being able to produce more than one’s own immediate needs lead to the emergence of barter. But with the introduction of money – which acts both, as a means of exchange, and a store of wealth – “excess productivity and production” could lead to the accumulation of “disposable income”; and it is this disposable income that drives an economy in 2 separate ways

- Consumption: disposable income drives trade, and thus economic activity.

- Investment; disposable income drives innovation, and thus economic complexity.

[Note: Complexity can be defined as “self-organized integrated diversity” and thus a “complex adaptive economy” is a highly diverse and integrated system.]

It is innovation that powers technological progress in society. While trade might grow the equilibrium size of an economy, it is innovation that drives the equilibrium complexity of an economy and thereby the complexity of society at large.

Allocation of Excess

At the core of laissez-faire economics is the idea that free markets are the optimal way to allocate resources in the economy. Adam Smith suggested that each individual knows how to best use one’s own time and money; and thus free markets are the optimal way to allocate resources in the economy. This idea should work equally well for both consumption and investment.

Excess resources drive growth. The allocation of one’s excess resources (i.e. excess productivity/ disposable income) to one’s own creative project is the basis of innovation. The allocation, of one’s excess resources, to somebody else’s creative project is the basis of investment. And from this, at the time, novel concept arose financial markets.

Financial Markets

Financial markets had been in existence (in crude form) for some time before the publication of Adam Smith’s work in 1776. In today’s modern financial world however “Capital Markets” have become the mechanism through which “the invisible hand” operates; and thus within mainstream economics free financial and capital markets are considered the optimal way to allocate savings to investments.

The market for savings and investments, however, are fundamentally different to most other markets. Most markets are consumer markets, operating in the price dimension (simply price discovery mechanisms), and deal in tangible things. Financial markets operate in the complexity and innovation dimension and deal in “ideas and expectations”!

Balance of Expectations

Built on the foundation of “the invisible hand” is “Efficient Market Hypothesis” (EMH). At the heart of EMH is the idea that that financial markets are a “fair game” in which buyers and sellers all have access to the same information and through their interaction they finds a price equilibrium which accurately reflects the markets “Balance of Expectations (BOE)”.

Wisdom of Crowds

The BOE is the “Wisdom of Crowds” in action. EMH suggests that in an efficient market the current market price is the right price, and future price moves should only ever occur when new information enters the market; consequently prices should simply follow a random path that reflects the random nature and occurrence of future news events.

Implicit to the idea of the “Wisdom of Crowds” is that no one player in the market might know all the available information, but the market as a whole does. Furthermore (and this is the contentious point about EHM), rational market expectations of unknown and unknowable future events are neither overly optimistic nor overly pessimistic.

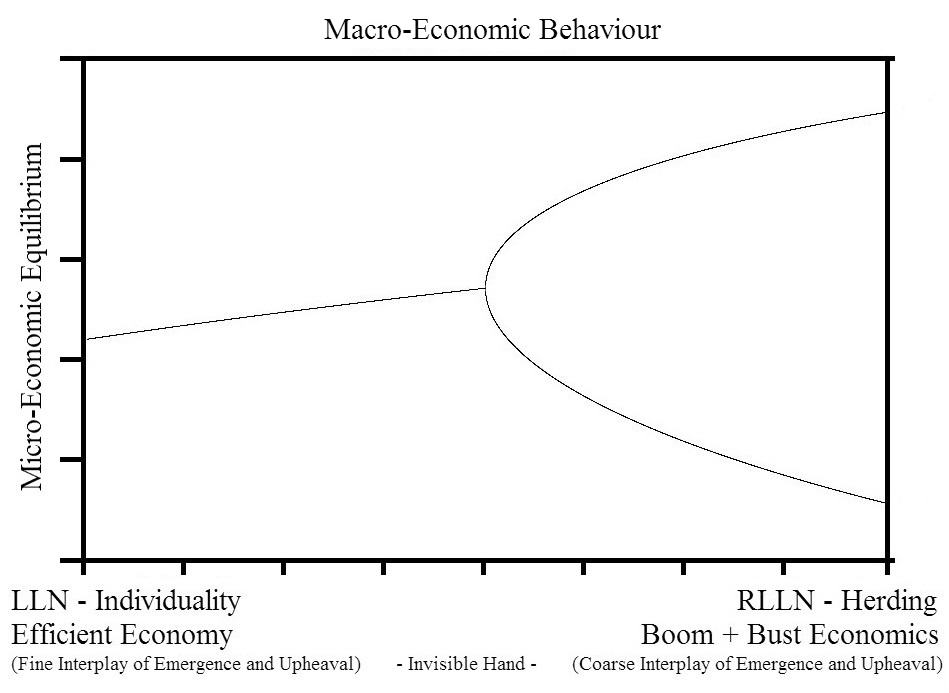

This apparent “rational wisdom” however, relies heavily on the “Law of Large Numbers” (LLN) …

LLN

The LLN is a statistical concept that deals with the idea that statistical accuracy is related to the size of the sample. Most people would recognize the central thesis: if you toss a coin four times, you won’t necessarily get a 50/50 split of heads and tails: indeed, you could get 4 tails, suggesting (wrongly) that the coin will always land on tails. But if you toss a coin a thousand times, you will get something close to a 50/50 split between heads and tails.

[Mathematically, it is expressed as: the Standard Deviation (of the Sample Average from the Expected Average) converges on zero as the Sample Size becomes infinitely large.]

Efficient markets thus rely on the fact that they are made up of very many independent players to ensure that there is a fairly even 50-50 split between those who think the next move is up, and those who think it is down. Or to put it another way: An efficient financial market relies on the Law of Large Numbers (LLN) to ensure that investment allocation decisions reflect a “realistic (BOE)”.

RLLN

Like any consumer market, an efficient financial market is supposed to be capable of self-stabilizing and thereby identifying a fair valuation, in a sterile and unemotional fashion, given all available information. Financial markets however are not sterile and unemotional. Financial markets are complex systems, full of adaptive agents, many of whom regularly deal in second-guessing the market’s expectations. Consequently every player in the market does not act autonomously; many follow the herd!

This tendency in financial markets towards herding behavior weakens the apparent wisdom of the crowd by reducing the large number of independent players in the market into smaller collective groups, and in so doing, effectively engineers a

“Reverse of the Law of Large Numbers” (RLLN)…

Inherent Vulnerability

This simple change for market players – from independent decision-makers (LLN) to collective groupthink (RLLN) – alters the mathematical probability of any market finding a stable equilibrium; and thus explains why financial markets don’t always do what they are supposed to do.

This inherent vulnerability to the emergence of herding and the RLLN means that:

The invisible hand (of the financial markets) is inherently vulnerable to the Emergence of Coarse Synchronicity and Chaos!

Part 4 – Critically Driven & Coarse Synchronization

Driven- Damped System

A CAE is a driven-damped system; driven by innovation and damped by natural entropic decay.

In this driven-damped system it is the constant “interplay” of these driving and damping forces that acts like “an invisible hand” both driving and fine-tuning Spontaneous Economic Self-Organization and the Emergence of Every Greater Economic Progress and Complexity.

Fundamentally though, the economy is a naturally damped system; meaning that if left undriven it will naturally decay – so ultimately the economy needs to be driven in order to simply stand still.

The job of financial markets is to ensure such sustaining investment in the economy is allocated to the right places. Moreover the markets can also allocate resources to new projects and ideas, and in so doing actually drive the economy forward (beyond the point of simply standing still) to greater heights and economic complexity (to the benefit of all – as Adam Smith suggested).

So given that Investment drives innovation and innovation drives economic progress and complexity, does this mean that ever greater investment automatically leads to ever greater economic progress and complexity?

Chaos Theory would suggest not. Chaos Theory suggests that there is an optimal “Rate of investment” in a CAE where the economy in capable of synchronizing investment with realistic business opportunities (beyond which coarse synchronicity sets in and investment is likely to be wasted).

Critically-Driven Economy

The investment of excess resources (beyond what is necessary to sustain the economy) drives competitive innovation, and innovation drives economic progress and complexity.

A complex economy is one where there is constant symbiotic balancing of competitive formation and selective dissolution leading to ever greater economic complexity. If the markets are doing their job correctly then a small level of excess investment will lead to the emergence of the most competitive innovation; however the downside to this meagre level of investment is that many good, and potentially very profitable, ideas get left unfunded.

The job of the capital markets is to identify the “optimal level of investment” by synchronizing the demand for investment opportunities with the supply of good ideas. An optimally efficient market is one that optimally drives the economy, a level of investment we could describe as “Critically-Driven Economics”.

A critically-driven economy however is an ideal which is rarely achieved…

Coarse Synchronization

In essence the critically-driven economy is one of “Accelerated Evolution”; an economy in which there is a constant interplay of the creative forces of innovation and upheaval; an optimally driven economy in which “The New” constantly replaces “The Old”.

Ideally the Invisible Hand will constantly fine-tune this optimal, complex, economic equilibrium by keeping investment in sync with supply of good ideas.

Fine-tuning to this optimal balance however means that the invisible hand relies very heavily on the LLN. Should herding in markets emerge, the RLLN will have the effect of bifurcating this balancing equilibrium of driving and damping forces, effectively moving demand for investment opportunities out of sync with the supply of good ideas….

So just as not enough money means that many good ideas go unfunded; too much investment means that a lot of investment resources get wasted on poor ideas, which will never realistically become viable self-sustaining and profitable businesses.

Herding invokes the RLLN, which weakens the fine-tuning abilities of the Invisible Hand. The emergence of the RLLN coverts fine-tuning to coarse-tuning causing markets to oscillate between under-driving and over-driving the underlying economy; which we witness as the behavior of the so-called “Business Cycle”.

Business Cycle

Investment may drive innovation, but not all investment leads to a self-reinforcing innovation (i.e. a self-funding business).

The business cycle equates to periods of economic trial and error. The cycle begins when societies as a whole start to self-organize an optimistic worldview. Banks lend more, as individuals and companies innovate. When competition becomes excessive however the self-organized optimism will ultimately fragment due to its inherent instability ushering in a period of collective self-organized pessimism as too many ideas ultimately fail the economic version of “Survival of the Fittest”.

Human beings are not machines nor totally rational, and as a result a critically-driven economy is an unlikely occurrence in a CAE. In reality most free market economies are more likely to be a naturally fluctuating system of “Innovation and Creative Destruction”.

What we want therefore, from any oversight of this system, is to ensure it is allowed to evolve unhindered through its natural spontaneous cycle. What we don’t want is to externally amplify the (the inherent vulnerability to the) RLLN; unfortunately, this is exactly what regularly happens!

Part 5 – Credit-Fuelled Chaos

Credit-Fuelled Booming Markets

Ideally an economy booming would be the result of strong economic development in both productivity and innovation. Unfortunately, in already developed economies this is usually not the case. Unfortunately, a boom in a developed economy is, more often than not, the result of a credit-fuelled excess of over-investment.

Easy access to credit, for creative business development, is the lifeblood of innovation; but easy access to credit, for asset price speculation on the other hand, is the fuel in the engine of a runaway market bubble.

Credit fuelled asset price speculation tends to massively amplify the RLLN in asset markets, turning a market price discovery mechanism from what is meant to be “The Wisdom of Crowds” into what appears to be “The Madness of Mobs”…

[The “Madness of Mobs” is the extreme of the RLLN in action. Mathematically the extreme of the RLLN occurs when the sample size does not head towards infinity but instead heads towards one. When the RLLN emerges the standard deviation does not converge to zero, but instead diverges and gets very, very large, causing the balanced distribution – guaranteed by the LLN – to eventually skew.]

Overstressing the System

Groupthink is okay in moderation, but too much of it will overstress the system. The access to credit for investment in asset markets can amplify the RLLN turning a normal, functioning, business cycle, into dysfunctional boom and bust cycle.

A normal business cycle is a cycle of investment of saved disposable income, but a boom and bust cycle is cycle of investment of saved disposable income AND borrowed future income!

The raison d’être of financial markets is to match savings to investments. Matching borrowings to investments is a preserve use of the system. Savings are disposable income not used for consumption. Borrowings are ongoing expenses that eat into non-disposable income (which might be otherwise used for consumption).

Most anyone who borrows to invest presumably does so believing that the investment will pay for itself; and often it does in the short term, but unfortunately usually not in the long term. In the meantime easy access to credit (this flood of extra money) can supercharge (the inherent vulnerability to herding in) booming asset markets.

Ponzi Scheme

Such inefficiency in financial markets are not good for the economy and certainly not good for society-at-large; inefficiency in financial markets usually mean that markets eventually start behaving like a ponzi scheme.

Rapidly rising asset markets are like a raging forest fire that constantly needs more fuel. In such markets this fuel ultimately comes from the weakest members of society. In the face of almost daily gains for everyone else, eventually everyone gets sucked in, even those who can’t afford it…

Banks fuel this Ponzi scheme by recklessly lending to the ever less creditworthy. This means that in this Ponzi scheme, as in all ponzi schemes, the poor are getting in last. Inefficient asset markets are consequently a very effective way of transferring money from the poor, and the not-so-rich, to the rich (and getting richer)…

Part 6 – Apparent Stability and Actual Stability

Economic Complexity is a process of the constant interplay of creative innovation and creative destruction. In a CAE, businesses and other economic entities, form and dissolve all the time – the whole never stays the same because the parts are constantly changing. So in a fast evolving economy it is, of course, no surprise when redundant things gradually disappear; but what is surprising, is when the whole economic system suddenly collapses.

Apparent Stability – Chaos hidden in the Order

In a normal functioning economy, many structures that are funded into existence don’t always remain in existence. If an emergence structure does not trade and integrate itself into the economy-at-large, it won’t be able to make profits and thereby self-reinforce.

In a dysfunctional economy however, many non-profitable entities can continue to survive well past their sell-by date. Such an economy might look stable on the surface but beneath the surface there lures an instability; an avalanche waiting to happen…

Often an economy that appears stable is in fact holding itself away from a less exalted equilibrium by sheer force of its own internal positive reinforcement. But there is potential for chaos to be hidden in the order, because such an unstable economy is vulnerable to collapse should the internal funding dynamics of the financial markets change.

The collapse of an economy artificially held away from a functional equilibrium can lead to sudden and violent change. Such upheavals are usually considered shocking and often described as freak events, but in truth there is in fact a mathematical “universality” in their occurrence that is only to be expected in complex systems where there is a constant interplay of the LLN and RLLN…

Actual Stability – Stagnation

In nature after such an evolutionary collapse, mother-nature will begin to rebuild, and in a normal business cycle so too would an economy. However in a boom and bust cycle things are not quite so easy!

Investments not funded out of savings, but funded out of future income continues to incur ongoing interest costs despite the fall in value of the investment. Not only that, but unfortunately for the borrower (and the economy at large), the principle also still needs to be repaid.

Thus an economic boom funded by credit, eats into disposable income long after the boom has completely disappeared. And since disposable income is what drives both investment and consumption, it depletion affects not only the growth of complexity in the economy but also the level of economic activity/trade and thereby the size of the economy as a whole.

In an economy the only time we really have stability is when nothing much is happening – and nothing much will happen when the driving force of the “Invisible Hand” is severely weakened.

With very little funding only the very best ideas get funded; but with no funding at all, and no consumer spending to boot, many existing businesses will likely decay. [In an economic bust, even healthy business go under; because a large amount of pre-existing disposable income is been redirected towards paying off debt.]

In a dysfunctional economy, the weight of unproductive debt substantially weakens the driving force of growth and innovation in a normal functional economy. Such an economy mired in debt will stagnate!

An economy devoid of disposable income is akin to a planet devoid of sunlight; nothing will grow!

Part 7 – Conclusion

Capitalism is perceived as the optimal growth engine of economic development and growth! Financial Markets are supposed to be the invisible hand that optimally allocates the supply of and demand for investment funds in a CAE. Chaos Theory alerts us however, to a possible vulnerability in the system…

The mathematics of chaos shows us that there is in fact an “Optimal Rate of Investment” in this Damped-Driven System – beyond which the system is vulnerable to “Coarse Synchronicity and Chaos”.

We know that, too much investment can overdrive the system causing the emergence of the so-called “business cycle”; excessive investment however has the effect of converting a functional cycle driven (even if slightly out of sync) by the LLN and “The Wisdom of Crowds”, finely balancing “Supply and Demand” (of investment funds); into a dysfunctional cycle driven by the RLLN and “The Madness of Mobs” coarsely balancing “Fear and Greed” (of a financial market gamble). What tips the system from one to the other (i.e. from functional to excessive) is when over-investment becomes “supercharged” by credit-fuelled investment.

Fundamentally, there are 5 levels of Driving Force in a Complex Adaptive Economy

- Minimum: Stops the natural decay of a naturally damping system.

- Small Excess: Under-Drives the Economy – a lot of good ideas are left unfunded.

- Critical Excess: Critically-Drives the Economy – optimally funds all the best ideas.

- Large Excess: Over-Drives the Economy into a “Business Cycle” – many poor ideas also get funded.

- Excessive Excess: Supercharges the Economy into a “Boom and Bust and Stagnation-Dead-End” – basically any idea will do.

Clearly credit is clearly the lifeblood of business and trade in the economy. Credit however has no place in the funding of asset price speculation. Excessive credit fuelled speculation is simply a build-up of instability in markets; an accident waiting to happen…

Financial markets are a CAS and thus not always efficient and often inherently unstable and are vulnerable to the RLLN. If we want these markets to operate in the most efficient fashion, we need to guard against any amplification of the RLLN; we need better control over the amount of credit in the system; both before and after a market bubble.

Vulnerability to the RLLN leads to the sub-optimal allocation of resources. The misallocation of savings and credit has 4 main effects:

- In the short term, it burns though savings wasting a valuable economic resource.

- In the long run, it starves good ideas of investment.

- It creates inequality, because bad investments always suck the poor in last, allowing the rich to get out…

- It creates suffocating debt, and with that debt, it sucks the driving force out of the economic system…

Complexity Theory shows us that the “optimal” Complex Adaptive Economy (CAE) self-organizes from the bottom up. Chaos shows us that there is an optimal rate of investment in a CAE – beyond which financial markets are vulnerable to “coarse synchronicity and chaos”.

Moreover the mathematics of chaos tells us that

“In the short term artificially pumped up asset markets, can have a trickle-down effect, but ultimately in the long term, the primary effect is to increase inequality.”

There has been a long running argument in economics as to whether an economy should be left alone or needs supervision. In a way both sides are right.

The economy is like a car, it has a battery, but we never use the battery when the car is running – the battery’s sole purpose in life is to kick-start the car into ignition. Using excessive credit in a booming economy is like using the battery while we are driving; lack of credit when the economy is stalled however is like trying to start the car without the ignition.

The takeaway message is that in any Driven-Damped Complex Adaptive System, positive feedback is always required in order for the system to be able to work its way away from the gravitational pull of natural spontaneous decay. In the push and pull of a Complex Adaptive Economy, a collapse in positive feedback can collapse the complex equilibrium which can mean that the “Business Cycle” itself effectively disappears. The takeaway message from this is

“Excessive Consumer Credit can overdrives an economy, but Excessive Consumer Debt can kill the drive altogether!”

So In Summary: We should treat the economy as we would a car – we should leave well alone when the engine is running and let the battery charge; but if the engine is stopped, then we have no option but to use the ignition…